This article focuses on a new, proactive approach to be well prepared for Camp Widowhood™, that new phase of life, where you get to deal with your personal grief and adjust nearly every aspect of your life. What this means is that instead of being numb and vulnerable, you will be better educated, organized and prepared for one of life’s inevitable transitions. The real benefit to you is the increased clarity about your new future, increased confidence about the decisions you will need to make and the peace of mind knowing you will take care of yourself and honor the commitments you’ve made to those you care about, as The Confident Widow™.

Note: “Widow” refers to both genders.

Years ago my clients referred me to their 45 year old friend, widowed for about a year. As we were preparing her net worth statement we came across the 1964 Red Chevrolet – our conversation seemed to stop. She stared at me…Is something wrong I asked? “I don’t know what to do with it…I’m afraid if I sell it Jack would get mad at me.” (Jack’s been dead for a year!) I thought, this poor woman, this is a real conversation she’s having with herself. And, had I been advising them while he was alive and asked him what she should do with the car if the proverbial bus hit him, he would’ve said, “Call my buddy Joe – he’s been bugging me about that car for years!” DONE!

I then visited my mother, a widow of 10 years and asked, “If you and dad could do it all over again, what do you wish you would have done differently?” Without hesitation, “I wish I had a better idea of what we had and that I knew more about our investments to understand why we owned particular stocks. I also wish I knew who he had been working with. When I look back, I was in shock the first 6 months after your father died, and when you’re in shock you can’t learn new things. I had insurance people, legal, investment, accounting, and social security people telling me what I should be doing and I found most of these interactions frustrating because I couldn’t fully comprehend what they were telling me. Sometimes I would say, ‘Well, if that’s what you think I should do, then I’ll do it.’” I thought, this state of mind is for the pits!

I then made sure both spouse clients were aware of their assets, liabilities, insurances, income sources, advisors, etc. But, I have recently discovered, it’s not sufficient… there are too many people unprepared for their new membership in Club Widowhood™ and I am doing something about it. I have decided to further elevate my deliverable with a step by step roadmap, The Confident Widow’s™ Roadmap, which is a proactive approach to help you be prepared should you outlive your spouse and reluctantly join Club Widowhood™.

The roadmap has seven primary sections to help you be prepared:

- Your alignment...to be a Confident Widow™.

- Your Awareness of...you! What to expect, emotions, health.

- A complete inventory of your advisors, documents, assets/liabilities, income/expenses.

- myDecision Free Zone™. Most of the 1st 12 month decisions will be made… Now! Whew!!!

- Cash Flow...where is it coming from and what do you need to know about investing your resources?

- Personal, relevant conversations.

- The Ultimate Dress Rehearsal!

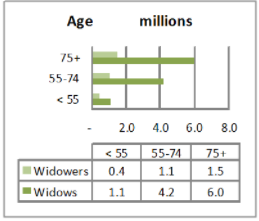

According to the 2010 U.S. Census Bureau, Widows outnumbered Widowers by a ratio of four to one.

It is my hope that spouses pursue their future with this statement: “My intent is to be a Confident Widow(er)™. What this means is that I will be educated, organized and prepared for Club Widowhood™. The real benefit is the increased clarity about my future, the increased confidence of where I am now and the increased capability to make smart decisions for myself and those I care about!” How about you?

About Patrick Bradley

Patrick Bradley is a financial consultant with more than 30 years of experience specializing in risk management, legacy planning and business continuity strategies. His commitment to helping others extends beyond his work and into his community where he is actively involved with multiple organizations. Learn more by visiting http://www.myFamilyCFO.net or connecting with Patrick on LinkedIn.

Disclosures: A Fixed Annuity is a long-term financial product designed largely for asset accumulation and retirement needs. Fixed Annuities generally contain fees and charges which include, but are not limited to, surrender charges, administrative fees and for optional contract riders and benefits. Withdrawals and death benefits are subject to income tax. If withdrawals and other distributions are received prior to age 59 ½, a 10% penalty may apply. Fixed Annuities typically carry surrender charges for several years that may be assessed against withdrawals. Certain Fixed Annuity product features, offered by some Fixed Annuity companies, such as stepped-up death benefit, a bonus credit and a guaranteed minimum income benefit, carry added fees. If you are investing in a Fixed Annuity through a tax-advantaged plan such as an IRA, you will get no added tax advantage. Under these circumstances you should only consider buying a Fixed Annuity if it makes sense because of the Fixed Annuities other features, such as lifetime income payments and death benefit protection. All guarantees of a Fixed Annuity are backed by the claims paying ability of the issuing insurer.